Charleston MLS Search & Local Market Experts | CharlestonHome.com

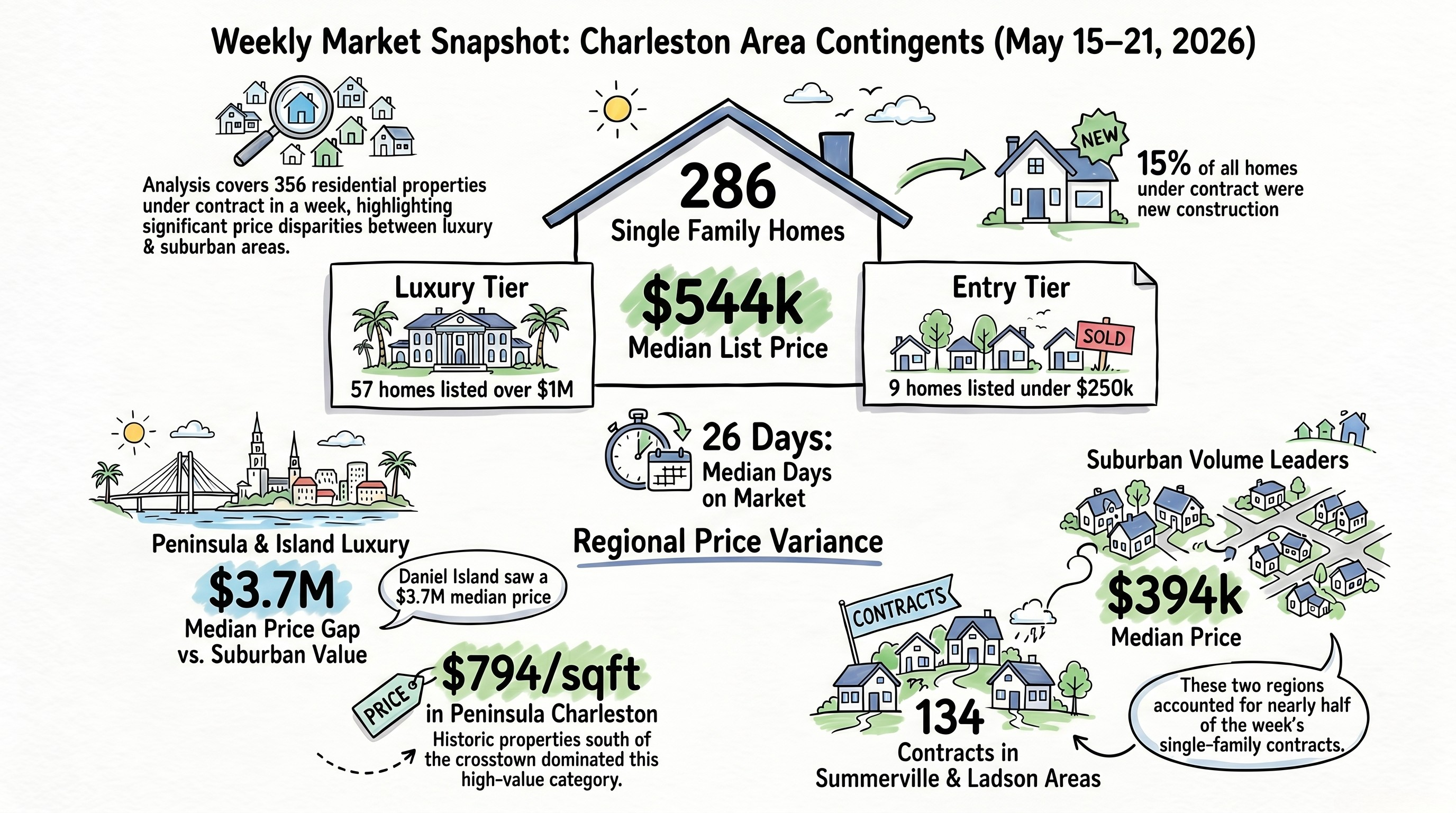

Single-family detached residences continue to serve as the primary economic engine of the lowcountry housing market, accounting for 286 of the week's total contracts.

I. Executive Market Summary

For the week of May 15th through May 21st, 2026, the Charleston market demonstrated robust demand and transactional velocity across diverse price points and submarkets, with a total of 356 residential properties moving to contingent/under-contract status.

II. Single-Family Home Market Overview

Single-family detached residences continue to serve as the primary economic engine of the lowcountry housing market, accounting for 286 of the week's total contracts.

Key Performance Indicators (KPIs)

- Median List Price: $544,000

- Median Price Per Square Foot: $248

- Median Continuous Days on Market (CDOM): 26 days (reflecting high liquidity for well-positioned inventory)

- Distressed Properties: Effectively negligible, accounting for just 2 out of 286 properties (0.7%), indicating exceptional market stability.

- New Construction Market Share: Represented a healthy 15% of all single-family contracts, acting as a crucial relief valve for inventory shortages.

The Luxury & Ultra-Luxury Tier

High-end real estate continues to see aggressive capital allocation. Of the single-family homes that went contingent:

- $1M+ Segment: 57 properties

- $2M+ Segment: 21 properties

- $3M+ Ultra-Luxury Segment: 16 properties

III. Regional Submarket Breakdown

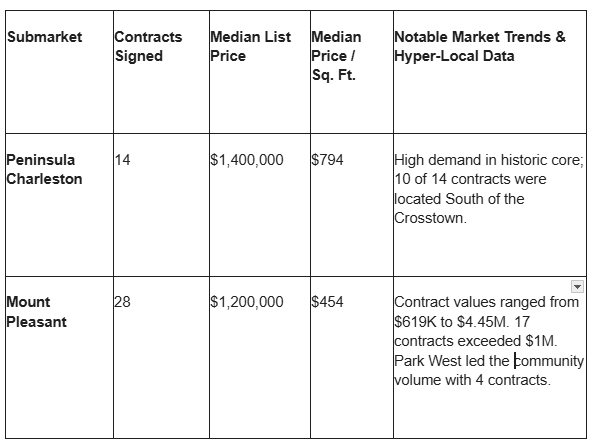

1. Premium Metro Core: Downtown & Mount Pleasant

These high-barrier-to-entry markets command the region's highest premiums due to historic significance, proximity to employers, and top-tier school districts.

2. The Islands: Premium Coastal Demand

The coastal island submarkets maintained high transactional volume last week, logging 49 single-family contracts across a mix of luxury master-planned communities and oceanfront enclaves.

- Daniel Island: Registered 7 contracts ranging from $1.45M to $6.9M. The submarket posted an ultra-premium median list price of $3,700,000 and $712/sqft.

- Johns Island: Led the islands in raw volume with 16 homes moving under contract. Activity was anchored by 4 new construction builds and 3 contracts within the Twin Lakes neighborhood. Median list price settled at $762,000 ($330/sqft).

- James Island: Logged 11 contingent contracts with a median list price of $645,000 ($411/sqft).

- Other Notable Coastal & Ultra-Luxury Sales: * Folly Beach: 3 contracts signed (ranging up to $1.7M)

- Edisto Beach: 6 contracts signed (ranging up to $1.95M)

- Wadmalaw Island: 2 contracts signed

- Marquee Ultra-Luxury Closings: Kiawah Island ($2.2M), Sullivan’s Island ($3.5M), Isle of Palms ($4.25M), and Seabrook Island ($4.85M).

3. Core Suburban Communities: West Ashley & North Charleston

These established communities offer a balanced blend of regional accessibility, strong neighborhood infrastructure, and varied price points.

- West Ashley: Sustained heavy volume with 37 homes going under contract, with the Carolina Bay development leading local activity (6 contracts). The median list price was $575,000 ($276/sqft), with 3 sales crossing into the million-dollar-plus luxury tier.

- North Charleston: Provided the region’s primary pocket of accessible metro pricing. The submarket recorded 15 contingent contracts with a median list price of $340,000 ($208/sqft), including 3 homes priced below $250,000.

4. Inland Corridors: High Volume & Volume New Construction

The highest raw contract volume in the tri-county area occurred in the inland suburbs. Driven heavily by national production builders and master-planned infrastructure, these areas absorb the bulk of the region's population growth.

- Hanahan / Goose Creek / Moncks Corner: Outpaced the entire Charleston region with 73 single-family contracts. New construction was the primary catalyst, accounting for 22 of those homes. The Cane Bay master-planned community alone accounted for 17 of the contracts. The median list price was $420,000 ($202/sqft).

- Summerville / Ladson: Posted 61 contracts, including 4 within the Sweetgrass Station community. New construction accounted for 5 of these homes, and the median list price stood at $394,000 ($207/sqft).

IV. The Condo & Townhome Market

For buyers seeking maintenance-free living or lower-barrier entry points into highly competitive zip codes, the attached-home sector remained highly liquid with 64 properties going under contract.

Price Bracket Distribution

- Under $300k: 17 units

- $300k–$499k (Bulk Market): 31 units

- $1.3M–$4.0M (Luxury Segment): 6 units

- New Construction Share: 7 units across the attached category

Expert Advisory Note

Real estate is fundamentally hyper-local. Macro statistics provide a helpful baseline, but factors like neighborhood-specific inventory constraints, school zoning changes, and seasonal demand shifting can dramatically alter your leverage at the negotiation table.

For personalized advisory services or a precise comparative market analysis (CMA) on your property, contact our advisory team directly at CharlestonHome.com.

Photo Gallery